Latest news from (Twitter)

Andrey Sizov

·

@sizov_andre

·

May 10

Retweeted...

Market Talk

·

@markettalkag

·

May 10

Today’s episode comes right after the May #WASDE reports. Join us for @PearsonCattle’s last day as our guest host to recap the report with @DuWayneBosse from @boltmarketing1 and more! #agtwitter

markettalkag.com/2024/05/10/fri…

markettalkag.com/2024/05/10/fri…

Market Talk

·

@markettalkag

·

May 10

Help us thank @PearsonCattle for filling in for @jesseallenag this week! We enjoyed having him on the show and for all the great conversation had on this busy week.

Karen Braun

·

@kannbwx

·

May 10

Looking at the last 5 weather headlines from the LSEG research team (as of Friday PM), the weather market could stay interesting in the coming weeks/months with continued S. Brazil flooding & dry center-west Brazil, and hot & dry threats to both USA & Black Sea growing regions.

Karen Braun

·

@kannbwx

·

May 10

May 10: Most-active CBOT #corn futures notch their highest settle of 2024 ($4.69-3/4 per bushel) as USDA pegs corn supplies below expectations.

Most-active corn had set a yearly high ($4.72) on Tuesday, though Dec corn has yet to return to its 2024 high ($5.02-1/4 set Jan. 2).

Most-active corn had set a yearly high ($4.72) on Tuesday, though Dec corn has yet to return to its 2024 high ($5.02-1/4 set Jan. 2).

Karen Braun

·

@kannbwx

·

May 10

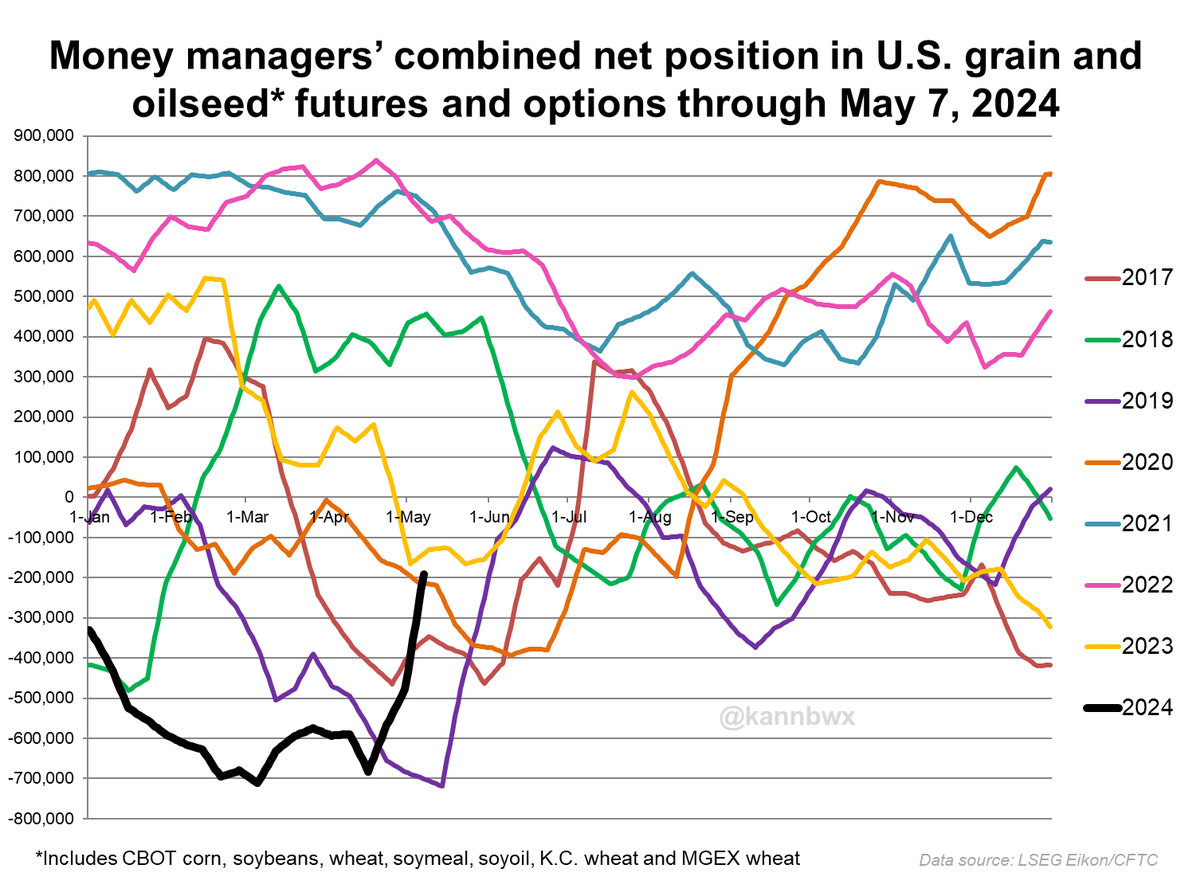

❌Speculators cover short bets

✅Speculators set short bets on FIRE in the week ended May 7 across U.S. grain & oilseed futures & options.

This was money managers' biggest week of collective net buying since July 2017.

✅Speculators set short bets on FIRE in the week ended May 7 across U.S. grain & oilseed futures & options.

This was money managers' biggest week of collective net buying since July 2017.

Arlan Suderman

·

@ArlanFF101

·

May 10

Retweeted...

Market Talk

·

@markettalkag

·

May 10

Market Talk

·

@markettalkag

·

May 10

Market Talk

·

@markettalkag

·

May 10

Hear #WASDE recap from Arlan Suderman (@ArlanFF101) from StoneX at the link below!

markettalk.libsyn.com/midday-comment…

markettalk.libsyn.com/midday-comment…

Andrey Sizov

·

@sizov_andre

·

May 10

Retweeted...

Andrey Sizov

·

@sizov_andre

·

May 10

Andrey Sizov

·

@sizov_andre

·

May 10

Andrey Sizov

·

@sizov_andre

·

May 10

Another gap up in Matif #wheat on Russian frosts last night (and CBOT rallied 20 cents). Overreaction or not? Farmers I spoke to are indeed concerned after the second cold night in a row...

Our take is in sizov.report update today.

#oatt #agwx #blacksea pic.twitter.com/83Cq7vMyli

Our take is in sizov.report update today.

#oatt #agwx #blacksea pic.twitter.com/83Cq7vMyli

Karen Braun

·

@kannbwx

·

May 10

Karen Braun

·

@kannbwx

·

May 10

Compared with demand, world #wheat supplies among major exporting countries are seen hitting 17-year lows in 2024/25. Stocks-to-use is pegged at 13.5%, near all-time lows.

Stocks-to-use in 2023/24 (14.7%) sits at a 16-year low but nearly identical to 2020/21.

Stocks-to-use in 2023/24 (14.7%) sits at a 16-year low but nearly identical to 2020/21.

Arlan Suderman

·

@ArlanFF101

·

May 10

Arlan Suderman

·

@ArlanFF101

·

May 10

Six months ago I started preparing our customers for the funds to exit short positions in grains by 2nd or 3rd qtr as reinflation expectations returned. That has happened, exiting us from the "commodity deflation" mantra of the past two years. #oatt

Arlan Suderman

·

@ArlanFF101

·

May 10

Today's response to the crop report is further evidence of the change in mindset toward commodities. Doesn't mean prices can't fall, but rising inflation expectations historically mean that the markets manage supply and demand at higher prices. Don't get greedy though. Still need… x.com/i/web/status/1…

Arlan Suderman

·

@ArlanFF101

·

May 10

Today's consumer sentiment index survey results showed that consumer expectations for longer-term inflation rose to 3.5% this month, up from 3.2% last month. Inflation expectations are rising. #oatt

Karen Braun

·

@kannbwx

·

May 10

In addition to USDA data, #China-U.S. trade relations are also in the news spotlight Friday as Biden is set to announce on Tuesday new tariffs on Chinese goods incl. EVs, solar & medical supplies. These tariffs will be on top of existing Trump-era ones.

yahoo.com/news/us-set-im…

yahoo.com/news/us-set-im…

Market Talk

·

@markettalkag

·

May 10

Hear #WASDE recap from Arlan Suderman (@ArlanFF101) from StoneX at the link below!

markettalk.libsyn.com/midday-comment…

markettalk.libsyn.com/midday-comment…

Market Talk

·

@markettalkag

·

May 10

Retweeted...

Arlan Suderman

·

@ArlanFF101

·

May 10

Still time to register for today's webinar that will be packed with USDA and weather analysis. #corn #soybeans #wheat #oatt stonex.cventevents.com/event/200327ce…

Market Talk

·

@markettalkag

·

May 10

Retweeted...

Karen Braun

·

@kannbwx

·

May 10

Karen Braun

·

@kannbwx

·

May 10

🇺🇸The 2024 U.S. #wheat harvest is seen slightly smaller than analysts thought but above last year's crop. Winter wheat output is up 2% year-on-year, HRW up 17%, SRW down 23%, white winter up 16%. The SRW number in particular was well below the average trade guess.

Andrey Sizov

·

@sizov_andre

·

May 10

Market Talk

·

@markettalkag

·

May 10

Retweeted...

Karen Braun

·

@kannbwx

·

May 10

Karen Braun

·

@kannbwx

·

May 10

Karen Braun

·

@kannbwx

·

May 10

🇺🇸The 2024 U.S. #wheat harvest is seen slightly smaller than analysts thought but above last year's crop. Winter wheat output is up 2% year-on-year, HRW up 17%, SRW down 23%, white winter up 16%. The SRW number in particular was well below the average trade guess. pic.twitter.com/7rlhqLssEC

Karen Braun

·

@kannbwx

·

May 10

Immediate report reaction: 2024/25 US/global corn supply is SIGNIFICANTLY less bearish than the market has braced for in recent months. Soybeans on the other hand...... 😬😬 Also, the wheat outlook isn't bearish with world stocks at multi-year lows. Would one call it bullish?

Market Talk

·

@markettalkag

·

May 10

On Friday, @USDA released the May WASDE report that could be construed as bearish for soybeans and neutral for corn and wheat.

markettalkag.com/2024/05/10/upc…

markettalkag.com/2024/05/10/upc…

Karen Braun

·

@kannbwx

·

May 10

Josh Linville

·

@JLinvilleFert

·

May 10

Closing out the week with pimping the newsletter!!

If interested, I go a lot deeper into price directions, market stories, outlooks, etc. in the farmer fertilizer newsletter. Tried to keep it as cheap as I could without getting in trouble!!

subscribe.stonex.com/farmer-fertili…

If interested, I go a lot deeper into price directions, market stories, outlooks, etc. in the farmer fertilizer newsletter. Tried to keep it as cheap as I could without getting in trouble!!

subscribe.stonex.com/farmer-fertili…

Andrey Sizov

·

@sizov_andre

·

May 10

Retweeted...

HL

·

@Lebcommodities

·

May 10

HL

·

@Lebcommodities

·

May 10

HL

·

@Lebcommodities

·

May 10

SovEcon analysts lowered their 2024 Russian wheat crop harvest forecast to 89.6 mmt, down from their 93.0 mmt forecast back in Apr' and below the 92.8 mmt harvested l/y.

Andrey Sizov

·

@sizov_andre

·

May 10

Retweeted...

Karen Braun

·

@kannbwx

·

May 10

Karen Braun

·

@kannbwx

·

May 10

All trade estimates for USDA's supply & demand reports due Friday at 11am CT. This is our first look at 2024/25, but there is still some interest in 2023/24, particularly in South America where weather/pests have stressed crops. US 2024/25 wheat crop will also be featured. pic.twitter.com/K6xONV11fw

Andrey Sizov

·

@sizov_andre

·

May 10

Below 90 mmt already

(But don't forget about historically high #wheat stocks, USDA carryout estimates are very misleading)

#russia #sizovreport x.com/cmdtySal/statu…

Sal

·

@cmdtySal

·

May 10

Sal

·

@cmdtySal

·

May 10

(But don't forget about historically high #wheat stocks, USDA carryout estimates are very misleading)

#russia #sizovreport x.com/cmdtySal/statu…

Sal

·

@cmdtySal

·

May 10

🇷🇺🌾Russian 12.5% wheat further bullish!

currently trading at $226 FOB!

Will production dip below 90MMT? cold temps and limited rainfall are setting the stage for a challenging #wheat growing season in #Russia!

#oatt #AgTwitter pic.twitter.com/JECT3JHab0

currently trading at $226 FOB!

Will production dip below 90MMT? cold temps and limited rainfall are setting the stage for a challenging #wheat growing season in #Russia!

#oatt #AgTwitter pic.twitter.com/JECT3JHab0

Arlan Suderman

·

@ArlanFF101

·

May 10

Market Talk

·

@markettalkag

·

May 10

Retweeted...

Karen Braun

·

@kannbwx

·

May 10

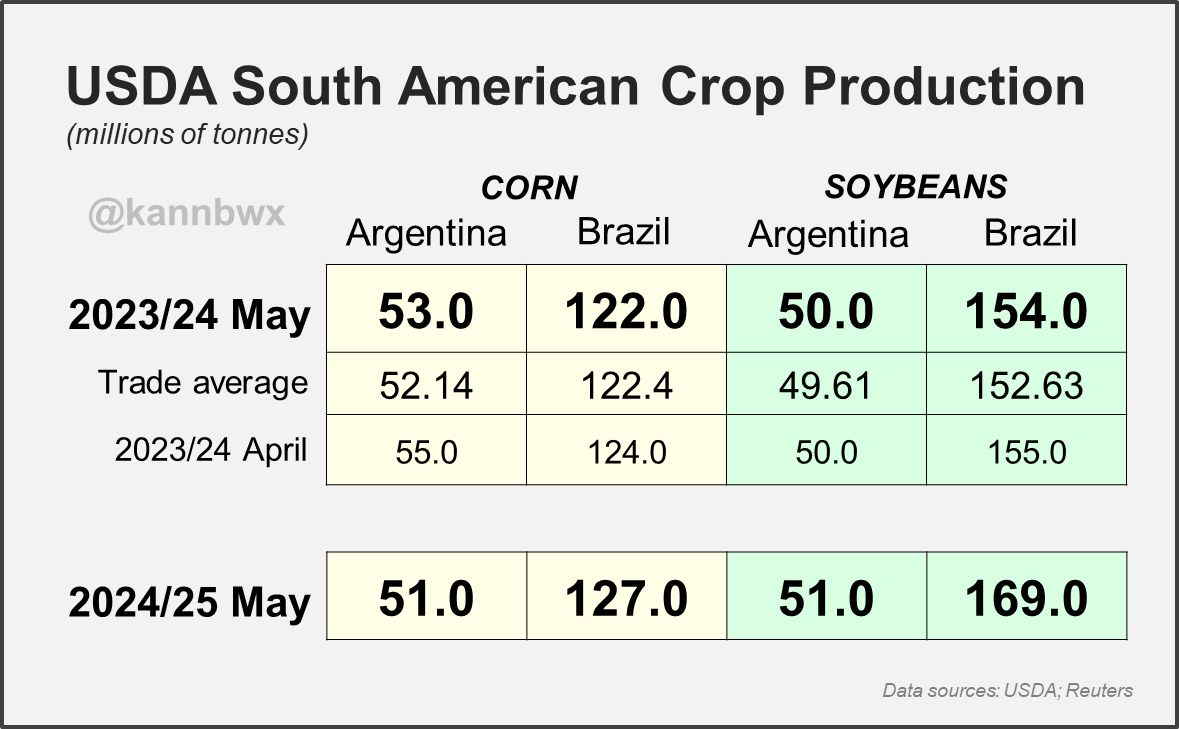

🇦🇷🇧🇷USDA trims 2023/24 outlooks for #Brazil & #Argentina #corn and Brazil #soybeans.

Record Brazilian soy crop seen in 2024/25, though Argy expectations are more modest.

Record Brazilian soy crop seen in 2024/25, though Argy expectations are more modest.

Arlan Suderman

·

@ArlanFF101

·

May 10

Market Talk

·

@markettalkag

·

May 10

Retweeted...

Karen Braun

·

@kannbwx

·

May 10

Karen Braun

·

@kannbwx

·

May 10

🇨🇳#China on Friday placed 2024/25 import estimates for #corn, #soybeans & #cotton well below 2023/24 levels on a large corn crop & reduced pig production capacity. 2024/25 estimates are (vs 23/24):

Corn 13 mmt (19.5 mmt)

Soy 94.6 mmt (96.1 mmt)

Cotton 2 mmt (2.8 mmt) pic.twitter.com/rTrgnVv8Ou

Corn 13 mmt (19.5 mmt)

Soy 94.6 mmt (96.1 mmt)

Cotton 2 mmt (2.8 mmt) pic.twitter.com/rTrgnVv8Ou

Arlan Suderman

·

@ArlanFF101

·

May 10

Market Talk

·

@markettalkag

·

May 10

Retweeted...

Market Talk

·

@markettalkag

·

May 10

Retweeted...

Arlan Suderman

·

@ArlanFF101

·

May 10

Karen Braun

·

@kannbwx

·

May 10

Arlan Suderman

·

@ArlanFF101

·

May 10

Market Talk

·

@markettalkag

·

May 10

Retweeted...

Arlan Suderman

·

@ArlanFF101

·

May 10

Market Talk

·

@markettalkag

·

May 10

Retweeted...

Karen Braun

·

@kannbwx

·

May 10

Karen Braun

·

@kannbwx

·

May 10

🇦🇷🇧🇷USDA trims 2023/24 outlooks for #Brazil & #Argentina #corn and Brazil #soybeans.

Record Brazilian soy crop seen in 2024/25, though Argy expectations are more modest. pic.twitter.com/hp3TOHXz6i

Record Brazilian soy crop seen in 2024/25, though Argy expectations are more modest. pic.twitter.com/hp3TOHXz6i

Market Talk

·

@markettalkag

·

May 10

Retweeted...

Karen Braun

·

@kannbwx

·

May 10

Karen Braun

·

@kannbwx

·

May 10

🇺🇸U.S. 2023/24 ending stocks come in at or below trade expectations, though 2024/25 #corn is below and #soybeans above. The projected year-on-year build in U.S. corn stocks is MUCH smaller than previously feared. pic.twitter.com/q44H0KNy31

Karen Braun

·

@kannbwx

·

May 10

All trade estimates for USDA's supply & demand reports due Friday at 11am CT. This is our first look at 2024/25, but there is still some interest in 2023/24, particularly in South America where weather/pests have stressed crops. US 2024/25 wheat crop will also be featured.

Andrey Sizov

·

@sizov_andre

·

May 10

Another gap up in Matif #wheat on Russian frosts last night (and CBOT rallied 20 cents). Overreaction or not? Farmers I spoke to are indeed concerned after the second cold night in a row...

Our take is in sizov.report update today.

#oatt #agwx #blacksea

Our take is in sizov.report update today.

#oatt #agwx #blacksea

Josh Linville

·

@JLinvilleFert

·

May 10

#farmer margins are looking pretty skinny this year. Next year not much better.

Time to get back to basics. At the core, farming is no more than input and output values.

Inputs - fert, chem, seed, etc.

Outputs - grain

The lower the value/ratio between the two, the better.

Time to get back to basics. At the core, farming is no more than input and output values.

Inputs - fert, chem, seed, etc.

Outputs - grain

The lower the value/ratio between the two, the better.

Karen Braun

·

@kannbwx

·

May 10

U.S. space weather forecasters have issued the first severe geomagnetic storm watch since 2005 after several strong solar flares this week. Impacts could start midday Friday and go thru Sunday. This could cause some power problems but will also offer aurora views to the lower US.

farmbucks.com

·

@farmbuckscom

·

May 10

Retweeted...

GrainStats 🌾

·

@GrainStats

·

May 9

GrainStats 🌾

·

@GrainStats

·

May 9

GrainStats 🌾

·

@GrainStats

·

May 9

☔️US Drought Monitor 🔥

Grain Production Areas Experiencing Drought (+/- weekly change)

🌽 Corn: 14% (-5%)

☁️ Cotton: 8% (+0%)

🌾 Sorghum: 53% (+3%)

🌱 Soybeans: 11% (-6%)

🌾 Spring Wheat: 15% (-12%)

🌾 Winter Wheat:… x.com/i/web/status/1… pic.twitter.com/drA8VJtflt

Grain Production Areas Experiencing Drought (+/- weekly change)

🌽 Corn: 14% (-5%)

☁️ Cotton: 8% (+0%)

🌾 Sorghum: 53% (+3%)

🌱 Soybeans: 11% (-6%)

🌾 Spring Wheat: 15% (-12%)

🌾 Winter Wheat:… x.com/i/web/status/1… pic.twitter.com/drA8VJtflt

Andrey Sizov

·

@sizov_andre

·

May 10

Where’s #corn and #soybeans reaction?

Reuters: U.S. President Joe Biden is set to announce new China tariffs next week targeting strategic sectors

…

Specific sectors were set to include electric vehicles, batteries and solar equipment

…

The measures could invite retaliation… x.com/i/web/status/1…

Reuters: U.S. President Joe Biden is set to announce new China tariffs next week targeting strategic sectors

…

Specific sectors were set to include electric vehicles, batteries and solar equipment

…

The measures could invite retaliation… x.com/i/web/status/1…

Andrey Sizov

·

@sizov_andre

·

May 10

Retweeted...

Andrey Sizov

·

@sizov_andre

·

May 10

Andrey Sizov

·

@sizov_andre

·

May 10

Where’s #corn and #soybeans reaction?

Reuters: U.S. President Joe Biden is set to announce new China tariffs next week targeting strategic sectors

…

Specific sectors were set to include electric vehicles, batteries and solar equipment

…

The measures could invite retaliation… x.com/i/web/status/1… pic.twitter.com/69dIFUFIIx

Reuters: U.S. President Joe Biden is set to announce new China tariffs next week targeting strategic sectors

…

Specific sectors were set to include electric vehicles, batteries and solar equipment

…

The measures could invite retaliation… x.com/i/web/status/1… pic.twitter.com/69dIFUFIIx

Andrey Sizov

·

@sizov_andre

·

May 10

Retweeted...

Andrey Sizov

·

@sizov_andre

·

May 9

Andrey Sizov

·

@sizov_andre

·

May 9

A few central Russian regions declared a state of emergency (SE) because of frosts.... To put that into perspective: there are 100+ events like that annually. Farmers need SE to get something from insurers.

#agwx #wheat x.com/sizov_andre/st…

#agwx #wheat x.com/sizov_andre/st…

Andrey Sizov

·

@sizov_andre

·

May 10

Retweeted...

Andrey Sizov

·

@sizov_andre

·

May 9

Andrey Sizov

·

@sizov_andre

·

May 9

For #wheat bull out there: a reminder that at this stage, light frosts (0/-1C) don't necessarily mean problems for the plants. Yes, the Center will have more cold temps next night as well.

A quick note has been posted for the clients: sizov.report/reports/22519/

#oatt #agwx pic.twitter.com/G0axavmfSB

A quick note has been posted for the clients: sizov.report/reports/22519/

#oatt #agwx pic.twitter.com/G0axavmfSB

Andrey Sizov

·

@sizov_andre

·

May 10

Smoking bad

Physics class good

(Something to show to your kids) x.com/humansnocontex…

humans without context

·

@HumansNoContext

·

May 10

humans without context

·

@HumansNoContext

·

May 10

Physics class good

(Something to show to your kids) x.com/humansnocontex…

humans without context

·

@HumansNoContext

·

May 10

Bro skipped physics class pic.twitter.com/1xA0MJnuRk

Josh Linville

·

@JLinvilleFert

·

May 9

Retweeted...

Market Talk

·

@markettalkag

·

May 9

Market Talk

·

@markettalkag

·

May 9

Join us for today's episode, one day ahead of the WASDE reports with @JLinvilleFert, VP of Fertilizer with @StoneX_Official and Bryan Doherty from @TotalFarmMktg. #agtwitter #markets

youtube.com/channel/UCQcS2…

youtube.com/channel/UCQcS2…

Andrey Sizov

·

@sizov_andre

·

May 9

Retweeted...

ian bremmer

·

@ianbremmer

·

May 9

ian bremmer

·

@ianbremmer

·

May 9

ian bremmer

·

@ianbremmer

·

May 9

much like what i say to my russian dissident friends:

steer clear of open windows pic.twitter.com/bOKvBBOcwl

steer clear of open windows pic.twitter.com/bOKvBBOcwl

Market Talk

·

@markettalkag

·

May 9

Join us for today's episode, one day ahead of the WASDE reports with @JLinvilleFert, VP of Fertilizer with @StoneX_Official and Bryan Doherty from @TotalFarmMktg. #agtwitter #markets

youtube.com/channel/UCQcS2…

youtube.com/channel/UCQcS2…

Karen Braun

·

@kannbwx

·

May 9

Josh Linville

·

@JLinvilleFert

·

May 9

Another slow day on the #fertilizer markets...and I'm loving it! After the last few years, some quiet periods are nice.

Only thing that would be better (from a farmer/retailer) POV would be lower prices!!!!

Only thing that would be better (from a farmer/retailer) POV would be lower prices!!!!

Andrey Sizov

·

@sizov_andre

·

May 9

🤔🤔🤔 x.com/kannbwx/status…

Karen Braun

·

@kannbwx

·

May 9

Karen Braun

·

@kannbwx

·

May 9

🇷🇺TASS quoting #Russia's ag ministry as saying "the killed crops will be replanted, all necessary resources are available for this" following emergency declarations in three grain regions over cold weather.

Is winter #wheat involved? Bit too late to replant that I'd guess... pic.twitter.com/dvGGmDtY9l

Is winter #wheat involved? Bit too late to replant that I'd guess... pic.twitter.com/dvGGmDtY9l

Andrey Sizov

·

@sizov_andre

·

May 9

Retweeted...

Not Jerome Powell

·

@alifarhat79

·

May 9

Not Jerome Powell

·

@alifarhat79

·

May 9

Not Jerome Powell

·

@alifarhat79

·

May 9

Just finished budgeting for the month pic.twitter.com/JyJnmAIAC8

Andrey Sizov

·

@sizov_andre

·

May 9

Retweeted...

Cornbelt Marketing, Inc. 🇺🇸

·

@SamuelBHudson

·

May 9

Cornbelt Marketing, Inc. 🇺🇸

·

@SamuelBHudson

·

May 9

Cornbelt Marketing, Inc. 🇺🇸

·

@SamuelBHudson

·

May 9

Have to respect chance for old crop #soybean export cuts in tomorrow's #WASDE. Running 6% behind on sales a/o week ending 5/2. Holding that pace into the end of the marketing year would pose a risk of eventually adding 100 mil bu back onto the BS. Just an observation... pic.twitter.com/wWuv27BVmU x.com/MSGCapital/sta…

Karen Braun

·

@kannbwx

·

May 9

🇦🇷Port & soy processing workers around #Argentina's Rosario hub are striking Thursday to protest harsh austerity measures implemented by President Milei. Rumors of this strike circulated last week and may have helped boost #soymeal futures even after the prior 2-day strike ended.

Andrey Sizov

·

@sizov_andre

·

May 9

Andrey Sizov

·

@sizov_andre

·

May 9

for some guys insisting on 6.5 zwn today....

#wheat #agwx x.com/CraigSolberg/s…

Craig Solberg

·

@CraigSolberg

·

May 9

Craig Solberg

·

@CraigSolberg

·

May 9

#wheat #agwx x.com/CraigSolberg/s…

Craig Solberg

·

@CraigSolberg

·

May 9

@sizov_andre Temperatures last night not even really comparable to what occurred last weekend pic.twitter.com/zHiGWGkyHT

Andrey Sizov

·

@sizov_andre

·

May 9

Reuters: #China approved the first gene-edited disease-resistant #wheat

We could see more of China's GE wheat varieties in the future, as it developed another variety with longer and heavier kernels and supposedly high yields earlier this year.

Wonder if one day Chinese… twitter.com/i/web/status/1…

We could see more of China's GE wheat varieties in the future, as it developed another variety with longer and heavier kernels and supposedly high yields earlier this year.

Wonder if one day Chinese… twitter.com/i/web/status/1…

Karen Braun

·

@kannbwx

·

May 9

Andrey Sizov

·

@sizov_andre

·

May 9

They need to add a button to eject the door... x.com/tunguz/status/…

Andrey Sizov

·

@sizov_andre

·

May 9

Retweeted...

Tatiana Stanovaya

·

@Stanovaya

·

May 9

Tatiana Stanovaya

·

@Stanovaya

·

May 9

Tatiana Stanovaya

·

@Stanovaya

·

May 9

Nobody in Moscow is looking for an exit strategy from the war or an opportunity to initiate dialogue with the West; nobody is concerned with persuading the West to ease sanctions; nobody is hungry for compromise with Ukraine, at least under its current leadership. There is no… twitter.com/i/web/status/1…

Andrey Sizov

·

@sizov_andre

·

May 9

Retweeted...

Visio-Crop

·

@VisioCrop

·

May 9

Visio-Crop

·

@VisioCrop

·

May 9

Visio-Crop

·

@VisioCrop

·

May 9

Info ou Intox sur coup de froid en Russie ?

Intox, juste de quoi faire bouillir la marmitte....

Ce n'est pas avec un petit -3°C sur du blé au stade BBBCH 29-31 voir 32 que cela va remettre en cause la production !

Bien d'accord avec @sizov_andre pic.twitter.com/RFal3lZpX3

Intox, juste de quoi faire bouillir la marmitte....

Ce n'est pas avec un petit -3°C sur du blé au stade BBBCH 29-31 voir 32 que cela va remettre en cause la production !

Bien d'accord avec @sizov_andre pic.twitter.com/RFal3lZpX3

Arlan Suderman

·

@ArlanFF101

·

May 9

Indicative of the continued tensions between China & the West. #oatt x.com/SkyNews/status…

Arlan Suderman

·

@ArlanFF101

·

May 9

Andrey Sizov

·

@sizov_andre

·

May 9

#Wheat market has misread last night's cold snap in Russia...and now it realizes that x.com/ArlanFF101/sta…

Andrey Sizov

·

@sizov_andre

·

May 9

#Wheat market has misread last night's cold snap in Russia...and now it's realizing that x.com/ArlanFF101/sta…

Andrey Sizov

·

@sizov_andre

·

May 9

The #wheat market has misread last night's cold snap in Russia...and now it's realizing that x.com/ArlanFF101/sta…

Andrey Sizov

·

@sizov_andre

·

May 9

A few central Russian regions declared a state of emergency (SE) because of frosts.... To put that into perspective: there are 100+ events like that annually. Farmers need SE to get something from insurers.

#agwx #wheat x.com/sizov_andre/st…

Andrey Sizov

·

@sizov_andre

·

May 9

#agwx #wheat x.com/sizov_andre/st…

Andrey Sizov

·

@sizov_andre

·

May 9

State of emergency has been declared in the Voronezh, Lipetsk, and Tambov regions due to frosts...

#wheat #agwx x.com/sovecon/status…

#wheat #agwx x.com/sovecon/status…

Arlan Suderman

·

@ArlanFF101

·

May 9

Arlan Suderman

·

@ArlanFF101

·

May 9

Marketing year to date grain sorghum export sales exceed the seasonal pace needed to hit USDA's target by 6 million bushels, down from 7 million the previous week. #oatt

Arlan Suderman

·

@ArlanFF101

·

May 9

Arlan Suderman

·

@ArlanFF101

·

May 9

#corn #oatt x.com/ScottIrwinUI/s…

Scott Irwin

·

@ScottIrwinUI

·

May 9

Scott Irwin

·

@ScottIrwinUI

·

May 9

Scott Irwin

·

@ScottIrwinUI

·

May 9

1. Earlier this week, I published a new FDD about the trend in the U.S. average corn yield. I concluded there is no compelling evidence that the historical two bushel rate of growth in corn trend yields in the U.S. has slowed in recent years. Have you ever wondered what drives… twitter.com/i/web/status/1…

Arlan Suderman

·

@ArlanFF101

·

May 9

#corn #oatt x.com/ScottIrwinUI/s…

Scott Irwin

·

@ScottIrwinUI

·

May 9

Scott Irwin

·

@ScottIrwinUI

·

May 9

2. When thinking about the drivers of corn trend yield increases the first thing that people usually think about is seed genetics, and that makes complete sense. But there other important factors. I wrote a new blog post about a factor that I think is… twitter.com/i/web/status/1…

Arlan Suderman

·

@ArlanFF101

·

May 9

#corn #oatt x.com/ScottIrwinUI/s…

Scott Irwin

·

@ScottIrwinUI

·

May 9

Scott Irwin

·

@ScottIrwinUI

·

May 9

5. I am going to go out on a limb and rank order what I think are the most important factors, including planters, in driving increased corn trend yields in the US the last couple of decades:

1. Improved seed genetics

2. Higher population

3. Better planter… twitter.com/i/web/status/1…

1. Improved seed genetics

2. Higher population

3. Better planter… twitter.com/i/web/status/1…

Arlan Suderman

·

@ArlanFF101

·

May 9

Arlan Suderman

·

@ArlanFF101

·

May 9

Arlan Suderman

·

@ArlanFF101

·

May 9

China was the featured buyer of US grain sorghum in the week ending May 2 at a net 5 million bushels, with roughly half of that a shift out of previous purchases by "unknown destinations." #oatt

Karen Braun

·

@kannbwx

·

May 9

USDA confirms the sale of 132,080 tonnes of U.S. #corn to Mexico. 61kt is for 2023/24 delivery and 71kt is for 2024/25.

Andrey Sizov

·

@sizov_andre

·

May 9

For #wheat bull out there: a reminder that at this stage, light frosts (0/-1C) don't necessarily mean problems for the plants. Yes, the Center will have more cold temps next night as well.

A quick note has been posted for the clients: sizov.report/reports/22519/

#oatt #agwx

A quick note has been posted for the clients: sizov.report/reports/22519/

#oatt #agwx

Andrey Sizov

·

@sizov_andre

·

May 9

State of emergency has been declared in the Voronezh, Lipetsk, and Tambov regions due to frosts...

#wheat #agwx x.com/sovecon/status…

SovEcon

·

@sovecon

·

May 9

SovEcon

·

@sovecon

·

May 9

#wheat #agwx x.com/sovecon/status…

SovEcon

·

@sovecon

·

May 9

State of emergency has been declared in the Voronezh, Lipetsk, and Tambov regions due to frosts on May 3-5 and May 8, which could damage crops.

More: blog.sizov.report/sovecon-russia…

#oatt #sizovreport

More: blog.sizov.report/sovecon-russia…

#oatt #sizovreport

Andrey Sizov

·

@sizov_andre

·

May 9

Retweeted...

CropProphet

·

@CropProphet

·

May 9

CropProphet

·

@CropProphet

·

May 9

CropProphet

·

@CropProphet

·

May 9

#Iowa #corn weighted drought was not eliminated, but it was substantially reduced because of recent rain. pic.twitter.com/BQvdvQ5VS6 x.com/CropProphet/st…

Andrey Sizov

·

@sizov_andre

·

May 9

Retweeted...

Karen Braun

·

@kannbwx

·

May 9

🌽2014 and 2024: twinning?

In ways, yes. New-crop CBOT #corn prices have been very similar between the two years and there are some overlapping fundamental themes.

But these two charts weaken the argument. Fund positioning and price trends since Jan. 1 have been opposite.

In ways, yes. New-crop CBOT #corn prices have been very similar between the two years and there are some overlapping fundamental themes.

But these two charts weaken the argument. Fund positioning and price trends since Jan. 1 have been opposite.

Andrey Sizov

·

@sizov_andre

·

May 9

Retweeted...

AMIS

·

@AMISoutlook

·

May 9

AMIS

·

@AMISoutlook

·

May 9

AMIS

·

@AMISoutlook

·

May 9

Russian farmers in the South, the nation's largest #wheat-growing and exporting region, reported a record-high wheat stock of 4.3 million metric tons as of April 1, marking an 8% increase year-on-year, as stated by SovEcon. twitter.com/sizov_andre/st…

Arlan Suderman

·

@ArlanFF101

·

May 9

Arlan Suderman

·

@ArlanFF101

·

May 9

Karen Braun

·

@kannbwx

·

May 9

Karen Braun

·

@kannbwx

·

May 8

🇦🇷Rosario grains exchange cuts #Argentina's #corn harvest to 47.5 mmt from 50.5 mmt a month ago on leafhopper damage. Rosario had previously pegged the crop at 57 mmt.

Andrey Sizov

·

@sizov_andre

·

May 9

Retweeted...

Andrey Sizov

·

@sizov_andre

·

May 8

Andrey Sizov

·

@sizov_andre

·

May 8

So #wheat importers are a bit short...GASC bought 420K vs. 120K at the previous tender in mid-April. The price is +~$23/mt.

#oatt #sizovreport #blacksea pic.twitter.com/EqJg2MKITc

#oatt #sizovreport #blacksea pic.twitter.com/EqJg2MKITc

Accounts we follow:

farmbucks.com

@farmbuckscom Leading-edge company in the #Grain #Marketplace. Changing the way #Farmers source grain prices.

@farmbuckscom Leading-edge company in the #Grain #Marketplace. Changing the way #Farmers source grain prices.

499 Following

·

554 Followers

Andrey Sizov

@sizov_andre I tweet about ag markets: wheat, corn, Black Sea. The best Black Sea wheat crop forecaster in 2022, 20, 19, 17; agtech enthusiast; ultramarathon runner

@sizov_andre I tweet about ag markets: wheat, corn, Black Sea. The best Black Sea wheat crop forecaster in 2022, 20, 19, 17; agtech enthusiast; ultramarathon runner

2128 Following

·

33.2K Followers

Karen Braun

@kannbwx Global Agriculture Columnist at Thomson Reuters. Meteorologist by training, gymnast for life. Views expressed are my own.

@kannbwx Global Agriculture Columnist at Thomson Reuters. Meteorologist by training, gymnast for life. Views expressed are my own.

147 Following

·

78.1K Followers

Arlan Suderman

@ArlanFF101 Chief Commodities Economist for StoneX Group, Inc. Tweets are my own and do not necessarily represent StoneX positions, strategies or opinions.

@ArlanFF101 Chief Commodities Economist for StoneX Group, Inc. Tweets are my own and do not necessarily represent StoneX positions, strategies or opinions.

4504 Following

·

48.5K Followers

Josh Linville

@JLinvilleFert Director of Fertilizer @StoneX_Official, 20 yrs experience in US/International Fertilizer Markets, All tweets are my own, RT≠Endorsements.

@JLinvilleFert Director of Fertilizer @StoneX_Official, 20 yrs experience in US/International Fertilizer Markets, All tweets are my own, RT≠Endorsements.

23.5K Following

·

34.7K Followers

Market Talk

@markettalkag Hosted by award winning farm broadcaster Jesse Allen (@jesseallenag). Tune in each weekday on YouTube, podcast and radio for market analysis and more!

@markettalkag Hosted by award winning farm broadcaster Jesse Allen (@jesseallenag). Tune in each weekday on YouTube, podcast and radio for market analysis and more!

342 Following

·

1430 Followers